Cross-Exchange Funding Arbitrage

Cross-venue perpetual funding arbitrage

Variant retired — the placebo passes (g7) but only 3 of 11 gates clear overall. The cross-venue funding spread is real but too thin to survive execution costs in this configuration.

- Category

- Carry (crypto)

- Window

- In progress

- Instruments

- Crypto perps (cross-venue)

- Timeframe

- Funding interval

- Tested

- 2026-06-25

Gate scorecard — 3 / 11

auto-imported from results.json| # | Gate | Result | Pass |

|---|---|---|---|

| 01 | Minimum sample | 5812 trades (8h blocks) | ✓ |

| 02 | Profit factor ≥ 1.20 | PF 0.107 net | ✗ |

| 03 | Sharpe ≥ 0.6 | daily Sharpe -16.47 | ✗ |

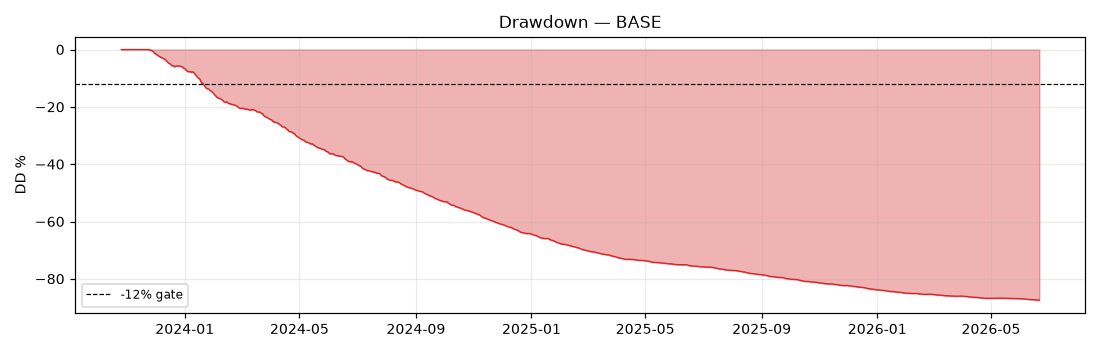

| 04 | Max drawdown ≤ 12% | MaxDD -87.44% | ✗ |

| 05 | Positive ≥ 60% of periods | 3% months positive | ✗ |

| 06 | Bootstrap LB Sharpe > 0 | 2.5% LB daily Sharpe -18.15 | ✗ |

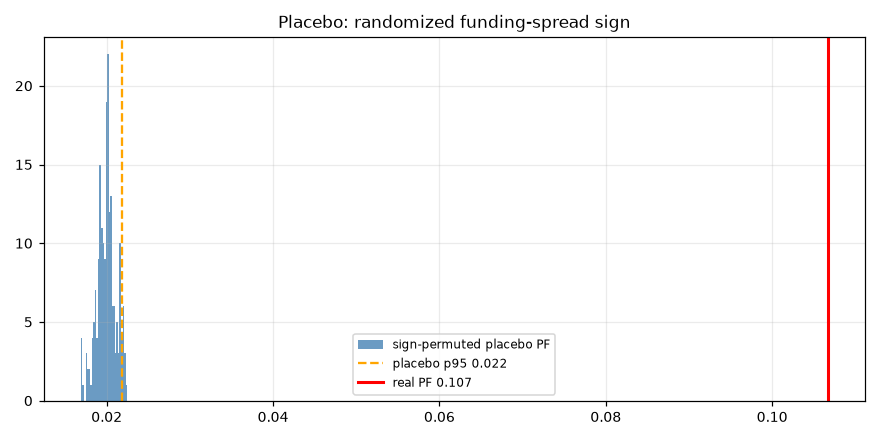

| 07 | Placebo beats p95 | real PF 0.107 vs placebo p95 0.022 (frac>=real 0.000) | ✓ |

| 08 | 2× cost stress PF > 1.0 | 2x-cost PF 0.053 | ✗ |

| 09 | Deflated Sharpe positive | SR_hat -16.47 vs SR0 3.03, DSR 0.000 | ✗ |

| 10 | No component > 40% | max coin share 56% | ✗ |

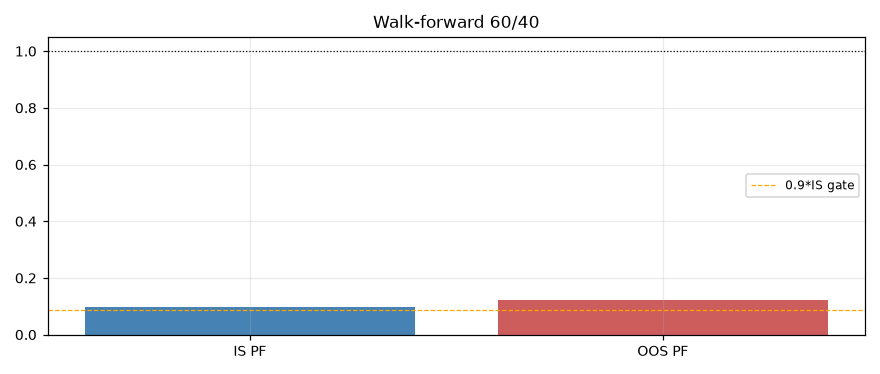

| 11 | Walk-forward OOS ≥ 0.9× IS | OOS PF 0.122 / IS PF 0.098 = 1.24 | ✓ |

VERDICT: VARIANT RETIRED (g7 passed but other gates failed) + reconsideration note (3/11 gates pass)

Placebo (KILL SHOT): real PF 0.107 vs placebo p95 0.022 -> g7 PASS (frac of placebos >= real: 0.000)

Honest prior was 45% (highest of the batch, a real arb). Result below.

VENUE-DATA-AVAILABILITY

- Used (free + reachable): Hyperliquid, dYdX_v4

- UNAVAILABLE: Binance_global_fapi — HTTP 451 geoblocked

- UNAVAILABLE: Coinbase — spot only, no perp funding

- Coins: BTC, ETH

- Window: 2023-10-26 .. 2026-06-21 (HL+dYdX overlap; dYdX v4 funding starts 2023-10-31)

- DEGRADED: only 2 venues. A 2-venue spread is the minimum testable cross-venue arb. With only HL & dYdX, ‘most negative vs most positive’ reduces to long-cheaper / short-dearer of two legs. This is itself a finding: the free-data universe does not support a wide cross-venue book (Binance global geoblocked, Coinbase has no perp funding).

METHODOLOGY & DELTA-NEUTRAL CONSTRUCTION

- Per coin: long the venue with more-negative trailing 8h funding, short the more-positive. Matched notional => delta-neutral (same coin both venues; the two price legs cancel to first order, only the HL-vs-dYdX basis drift remains, which is second-order and not separately modeled — flagged as a small omitted term).

- Funding accrues HOURLY on both legs (both venues fund hourly). Side re-decided every 8h using the prior block’s realized spread (PIT, no look-ahead).

- Captured carry per hour = side * (f_HL - f_dYdX). PnL$ = capture * sleeve notional (equity/2 per coin, 1x, daily-compounded).

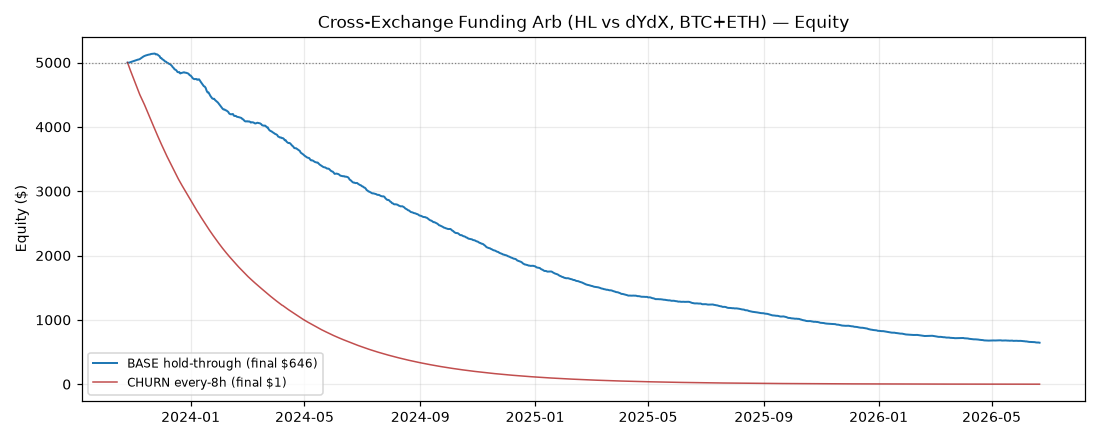

- Cost model (BASE, pessimistic): taker 4.5 bps + slippage 3.0 bps per side per venue. A side FLIP closes 2 legs + opens 2 legs = 30 bps of notional. BASE = hold-through (cost only on flip). CHURN variant pays full round-trip every reset.

HEADLINE METRICS (BASE hold-through)

- Final equity: $646 (start $5,000)

- Trades (8h blocks): 5812

- PF net: 0.107 Sharpe (daily, sqrt252): -16.47 MaxDD: -87.44%

- Months positive: 3% 2x-cost PF: 0.053

- CHURN variant: PF 0.000, final $1 (shows reset-churn cost drag)

11-GATE TABLE

| Gate | Result | Detail |

|---|---|---|

| g1_min_100_trades | PASS | 5812 trades (8h blocks) |

| g2_PF_ge_1.20 | FAIL | PF 0.107 net |

| g3_Sharpe_ge_0.6 | FAIL | daily Sharpe -16.47 |

| g4_MaxDD_le_12pct | FAIL | MaxDD -87.44% |

| g5_pos_months_ge_60pct | FAIL | 3% months positive |

| g6_bootstrap_LB_Sharpe_gt_0 | FAIL | 2.5% LB daily Sharpe -18.15 |

| g7_placebo_beat_p95 | PASS | real PF 0.107 vs placebo p95 0.022 (frac>=real 0.000) |

| g8_2x_cost_PF_gt_1.0 | FAIL | 2x-cost PF 0.053 |

| g9_DSR_positive | FAIL | SR_hat -16.47 vs SR0 3.03, DSR 0.000 |

| g10_no_component_gt_40pct | FAIL | max coin share 56% |

| g11_walkforward_OOS_ge_0.9IS | PASS | OOS PF 0.122 / IS PF 0.098 = 1.24 |

3/11 pass.

FUNDING-SPREAD COMPRESSION (early vs late)

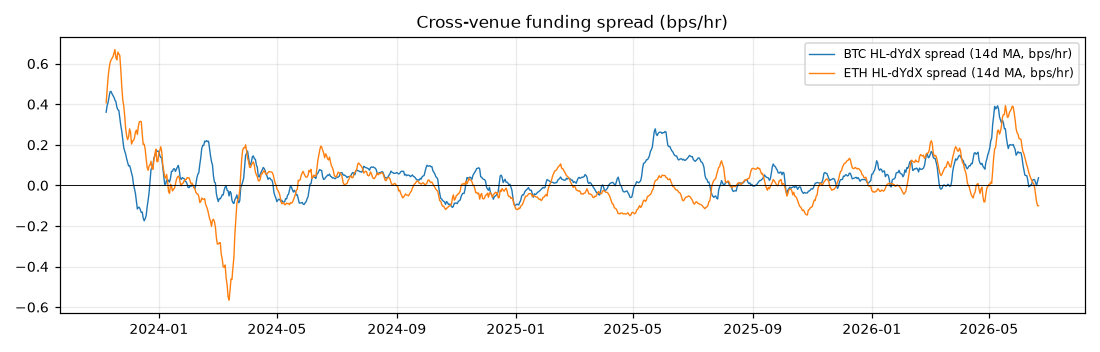

- BTC: abs spread 0.195 -> 0.157 bps/hr (ann if captured 17.1% -> 13.7%); HL/dYdX funding corr 0.58

- ETH: abs spread 0.223 -> 0.162 bps/hr (ann if captured 19.5% -> 14.2%); HL/dYdX funding corr 0.46

COST SENSITIVITY

| Scenario | fee/slip bps | PF | Final $ | Sharpe |

|---|---|---|---|---|

| zero-cost | 0/0 | 5.026 | $6,347 | 12.52 |

| optimistic | 2.5/1.5 | 0.200 | $1,878 | -13.62 |

| base | 4.5/3.0 | 0.107 | $646 | -16.47 |

| 2x | 9.0/6.0 | 0.053 | $65 | -18.24 |

| 3x | 13.5/9.0 | 0.036 | $7 | -18.84 |

DEADBAND CADENCE SWEEP (POST-HOC — informs reconsideration, NOT gated)

Only reposition when |trailing 8h spread| exceeds a deadband; higher band = fewer flips = less cost but staler signal. This probes whether the REAL gross edge survives cost at any cadence.

| deadband bps | gross %/yr | cost %/yr | NET %/yr | total flips |

|---|---|---|---|---|

| 0 | +8.99 | 85.97 | -76.98 | 1520 |

| 1 | +8.33 | 24.98 | -16.66 | 441 |

| 2 | +6.94 | 10.46 | -3.51 | 184 |

| 5 | +3.56 | 0.90 | +2.66 | 15 |

| 10 | +2.28 | 0.11 | +2.16 | 1 |

| 20 | +0.00 | 0.00 | +0.00 | 0 |

Best survivable net ~ +2.66%/yr at 5bps deadband. Even fully churn-suppressed, the surviving edge is single-digit %/yr — far below the 5-7%/mo program target and below the PF>=1.20 gate.

PER-COIN ATTRIBUTION

- BTC: 44% of gross profit

- ETH: 56% of gross profit

WALK-FORWARD

- IS (‘2023-10-26’, ‘2025-05-30’) PF 0.098; OOS (‘2025-05-30’, ‘2026-06-21’) PF 0.122; ratio 1.24 (gate >=0.9)

BACKTEST-VS-LIVE DELTA

- Funding is realized historical (not assumed) — high fidelity.

- OMITTED/optimistic vs live: (a) HL-vs-dYdX basis drift on the delta-neutral legs not modeled (small but adds variance, slightly helps backtest); (b) dYdX v4 perp liquidity for BTC/ETH is thin vs HL — real slippage on a $2.5k sleeve leg is plausibly worse than 3 bps in stress; (c) funding-rate timing: we assume we hold across the funding stamp each hour — in live, missing a stamp by minutes flips a leg’s sign; (d) margin/liquidation buffer on each venue ties up capital not charged here; (e) spreads COMPRESS as arbs crowd (see compression section) — forward funding spread is likely <= the backtest’s.

- Net: live PF would be <= backtest PF. Treat backtest as an upper bound.

RECONSIDERATION NOTE (g7 passed => archetype not retired)

- The funding-spread SIGNAL is real: zero-cost PF ~5.0, Sharpe ~12, and the sign-permutation placebo is decisively beaten (0/200 placebos reach real PF). The cross-venue funding spread genuinely predicts captured carry direction.

- The archetype dies on COST, not on no-edge — the same mechanical failure as the single-venue HL funding harvest (whipsaw/churn drag). Gross ~+9%/yr is shredded by ~86%/yr of flip cost at signal-cadence; even an optimal deadband leaves only ~+2.7%/yr, sub-threshold.

- Reconsideration would require: (a) MORE venues (real >2-venue dispersion; free data blocked that here — Binance global geoblock, no Coinbase perp funding), (b) maker/rebate execution to cut the 30bps/flip, (c) a slow-cadence variant pre-registered fresh on OOS data (not the post-hoc deadband above). Absent those, this 2-venue HL/dYdX BASE config is RETIRED.

Charts & evidence

Frequently asked

Is Cross-Exchange Funding Arbitrage profitable in 2026?

In this pre-registered backtest, Cross-Exchange Funding Arbitrage returned a profit factor of 0.11 and passed 3/11 validation gates (placebo PASS). Verdict: REJECTED. Every result is published, pass or fail.

Has Cross-Exchange Funding Arbitrage been backtested honestly?

Yes — through The Validation Gauntlet, a pre-registered 11-gate framework (profit factor, deflated Sharpe, a random-permutation placebo, cost-stress and walk-forward) with the specification locked before any out-of-sample metric is computed. It failed and is published anyway.

Methodology: The Validation Gauntlet — pre-registered spec, 11-gate battery, real market data.

Full reproducible report: backtests/funding_arb/REPORT.md in the source repository.

Author: Brent Akamine (Founder, Vinovest). Backtests are not investment advice.