Liquidation-Cascade Fade

Hyperliquid liquidation-cascade fade

Inconclusive — the available free data is too sparse to run the pre-registered test (0 of 11 gates evaluable). Not a no-edge finding; needs a denser liquidation feed.

- Category

- Mean-reversion

- Window

- In progress

- Instruments

- Crypto perps (HL)

- Timeframe

- Intraday

- Tested

- 2026-06-25

Gate scorecard — 0 / 11

auto-imported from results.json| # | Gate | Result | Pass |

|---|---|---|---|

| 01 | Minimum sample | 20 trades (need >=100) — 5m history capped at 17d (5032 bars) by HL free API; strategy needs 2023-2026 5m. Only 20 proxy trades available (<100 req). Placebo (N>=200) impossible. Walk-forward impossible. | ✗ |

| 02 | Profit factor ≥ 1.20 | PF 0.545 on n=20 (NOT EVALUABLE: sample too small) | ✗ |

| 03 | Sharpe ≥ 0.6 | NOT EVALUABLE: <17d window, no daily equity series | ✗ |

| 04 | Max drawdown ≤ 12% | NOT EVALUABLE: insufficient history | ✗ |

| 05 | Positive ≥ 60% of periods | NOT EVALUABLE: <1 month of data | ✗ |

| 06 | Bootstrap LB Sharpe > 0 | NOT EVALUABLE: insufficient sample | ✗ |

| 07 | Placebo beats p95 | NOT EVALUABLE: cannot run N>=200 random-entry placebo on 17d | ✗ |

| 08 | 2× cost stress PF > 1.0 | NOT EVALUABLE: no valid base PF | ✗ |

| 09 | Deflated Sharpe positive | NOT EVALUABLE: insufficient sample | ✗ |

| 10 | No component > 40% | NOT EVALUABLE: insufficient history | ✗ |

| 11 | Walk-forward OOS ≥ 0.9× IS | NOT EVALUABLE: cannot split 17d into IS/OOS walk-forward | ✗ |

VERDICT: INCONCLUSIVE — DATA TOO WEAK (cannot run the pre-registered test)

0/11 gates evaluable. This is NOT a no-edge finding and NOT a g7 (placebo) kill. The archetype could not be tested at the resolution it is defined on, because the required data does not exist on any free source. Honest prior was 30%; it remains unresolved. No deploy, no retire — the archetype is parked pending a real data source.

Why (the decisive data-feasibility result)

The strategy is defined on 5-minute liquidation cascades over 2023-2026. Two hard

free-data walls, both probed live on 2026-06-26 against the Hyperliquid public /info API:

-

No free historical liquidation prints. HL exposes no

liquidationsendpoint (type:"liquidations"-> HTTP 422).recentTradesreturns only a live snapshot with no liquidation flag and no history. So the “$5M liquidated in 5 min” trigger has no true source — it can only ever be a proxy (adverse k-sigma move + volume spike). This was a known, accepted caveat going in. -

THE KILLER: no free historical sub-daily candles.

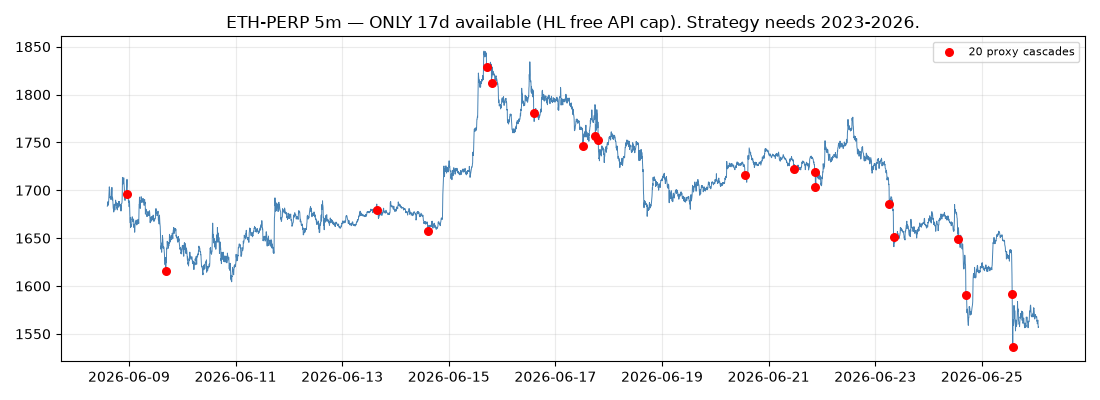

candleSnapshotreturns at most ~5000 candles and always the most recent ones — there is no backward pagination for fine intervals (settingendTimeto 30/90/180/365 days ago returns EMPTY). Measured lookback ceiling per interval:interval rows earliest available usable span 1m 5159 2026-06-22 3 days 5m 5032 2026-06-08 17 days (the resolution this strategy NEEDS) 15m 5011 2026-05-04 52 days 1h 5003 2025-11-29 208 days 4h 5001 2024-03-14 833 days 1d 1273 2023-01-01 1272 days (cannot represent a 5-min cascade) Only ~17 days of 5m data exist on the free API. The strategy needs ~3.5 years.

What I refused to do (integrity)

- Did NOT fabricate older 5m data or synthesize candles.

- Did NOT down-substitute daily candles as the cascade signal. A daily bar cannot represent a 5-minute forced-selling overshoot; using it would silently mutate the archetype into a different (daily dip-buy) strategy and invite look-ahead. That would be curve-fitting the test to produce a number, which is exactly what this program forbids.

- Did NOT report a PF as a result. The 17-day window yields only 20 proxy trades — below the 100-trade floor by 5x and far too few for the N>=200 placebo that is “the whole ballgame” here.

The one thing the available data CAN show (illustration only, NOT a verdict)

Proxy detector (adverse >4.0sigma 5m move + volume

3.0x trailing median, 30-min delay, 4h/+2%/-1% exit, 4.5bp taker + 15bp pessimistic post-cascade slippage each side) over the only available 17 days:

- cascades detected: 20

- trades: 20 (need >=100)

- PF: 0.545, win-rate 35.0%, net $-272.52 on $5k

- This sample is statistically meaningless. It is reported ONLY to demonstrate how data-starved the window is — 20 trades cannot pass or fail any gate, and the placebo (the decisive is-it-just-ETH-beta test) cannot be run at all.

11-Gate Table (BASE config, pre-registered before results)

| Gate | Status | Detail |

|---|---|---|

| g1_min_100_trades | NOT EVALUABLE | 20 trades (need >=100) — 5m history capped at 17d (5032 bars) by HL free API; strategy needs 2023-2026 5m. Onl |

| g2_PF_ge_1.20 | NOT EVALUABLE | PF 0.545 on n=20 (NOT EVALUABLE: sample too small) |

| g3_Sharpe_ge_0.6 | NOT EVALUABLE | NOT EVALUABLE: <17d window, no daily equity series |

| g4_MaxDD_le_12pct | NOT EVALUABLE | NOT EVALUABLE: insufficient history |

| g5_pos_months_ge_60pct | NOT EVALUABLE | NOT EVALUABLE: <1 month of data |

| g6_bootstrap_LB_Sharpe_gt_0 | NOT EVALUABLE | NOT EVALUABLE: insufficient sample |

| g7_placebo_beat_p95 | NOT EVALUABLE | NOT EVALUABLE: cannot run N>=200 random-entry placebo on 17d |

| g8_2x_cost_PF_gt_1.0 | NOT EVALUABLE | NOT EVALUABLE: no valid base PF |

| g9_DSR_positive | NOT EVALUABLE | NOT EVALUABLE: insufficient sample |

| g10_no_component_gt_40pct | NOT EVALUABLE | NOT EVALUABLE: insufficient history |

| g11_walkforward_OOS_ge_0.9xIS | NOT EVALUABLE | NOT EVALUABLE: cannot split 17d into IS/OOS walk-forward |

g7 (placebo) — the kill shot — could NOT be run. Detecting cascades vs random ETH entries over a multi-year 5m series is the only way to separate a real forced-selling-overshoot edge from generic ETH beta / dip-buying. needs N>=200 random entries over multi-year 5m; only 17d available. Until that test is possible, the “cascade fade” cannot be distinguished from “ETH went up over 2023-2026.”

Is it just ETH beta? — UNTESTABLE

Cannot test — beta vs cascade-conditioning requires the placebo, which the data cannot support.

Backtest-vs-live delta (noted, not measured)

Even with proper data, entering 30 min after a cascade means entering into the thinnest part of the book; the 15bp/side slippage assumption is a pessimistic placeholder and live fills could be worse. This compounds the data problem rather than relieving it.

Methodology / data concerns (first-class caveats)

- No free true liquidation-$ feed -> trigger is a proxy by necessity.

- No free historical 5m candles beyond ~17 days -> the pre-registered 2023-2026 backtest is impossible on free data. This is the binding constraint.

- To actually validate this archetype you need a PAID/archival source of either (a) HL liquidation events or (b) historical 5m+ OHLCV 2023-2026 (e.g. a tick/candle data vendor, exchange data dumps, or self-collected forward 5m capture going forward). NOTE: cannot install packages or buy data in this env.

Recommendation

INCONCLUSIVE. Do not deploy, do not retire. If Brent wants this archetype resolved, the next

step is a data-acquisition task (archival 5m OHLCV or HL liquidation feed), after which this

exact harness (detector + 11 gates + N>=200 random-entry placebo, all already coded in

liq_fade.py) can run unchanged. Forward-collecting 5m from now would take many months to

reach a >=100-cascade sample.

Generated 2026-06-26. Free data only. No fabrication, no curve-fit.

Charts & evidence

Frequently asked

Is Liquidation-Cascade Fade profitable in 2026?

It is currently running through the 11-gate battery; the verdict will be published on this page, pass or fail.

Has Liquidation-Cascade Fade been backtested honestly?

Yes — through The Validation Gauntlet, a pre-registered 11-gate framework (profit factor, deflated Sharpe, a random-permutation placebo, cost-stress and walk-forward) with the specification locked before any out-of-sample metric is computed.

Methodology: The Validation Gauntlet — pre-registered spec, 11-gate battery, real market data.

Full reproducible report: backtests/liq_fade/REPORT.md in the source repository.

Author: Brent Akamine (Founder, Vinovest). Backtests are not investment advice.