Crabel NR7 Breakout (XAUUSD)

Narrow-Range-7 volatility-compression breakout

Passes 4 of 11 gates. The NR7 compression signal beats a random placebo (real PF 0.643 vs placebo p95 0.336) and walk-forward holds — but it is firmly unprofitable net of costs on gold: Sharpe −0.83, max drawdown −50.5%, positive in only 20% of years.

- Category

- Volatility breakout

- Window

- 2017–2026 (XAUUSD)

- Instruments

- XAUUSD (gold)

- Timeframe

- Daily (NR7 trigger, intraday breakout)

- Tested

- 2026-06-25

The story in one line

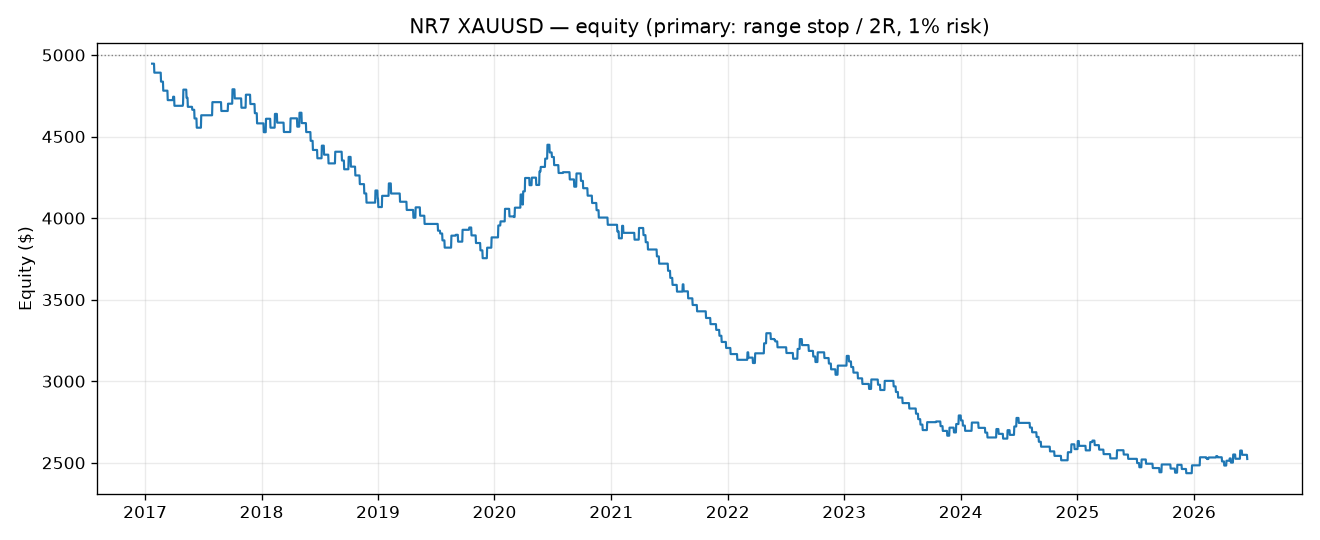

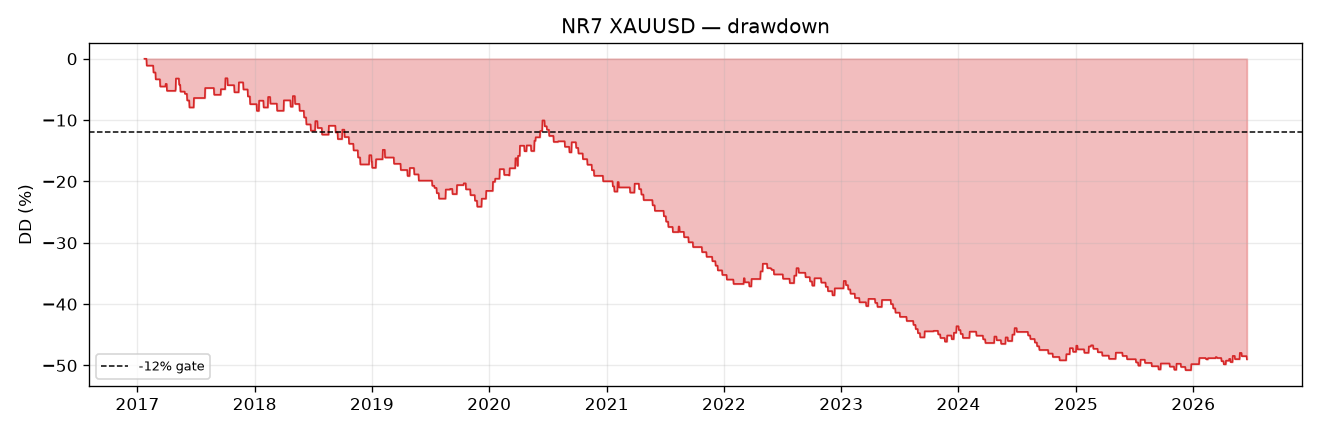

Toby Crabel’s Narrow-Range-7 breakout — buy/sell the break of the bar with the tightest range of the last seven, stop on the opposite side, 2R target — was run on gold (XAUUSD) over 2017–2026 through a pre-registered 11-gate battery. It passes 4 of 11 gates and ends at $2,523 from a $5,000 start (−50%), profit factor 0.643, Sharpe −0.83, max drawdown −50.5%, positive in only 20% of years.

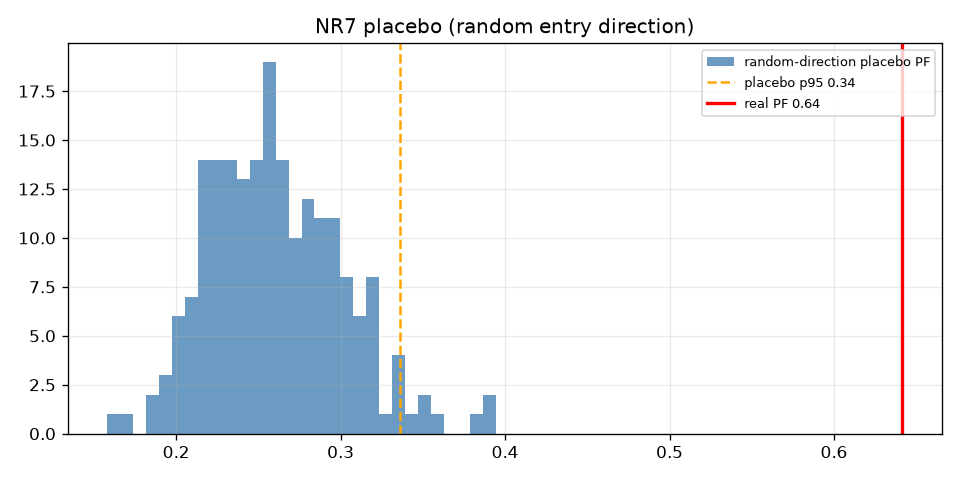

The interesting part: the compression signal is real. NR7 clears the placebo gate — real PF 0.643 beats the random-permutation 95th percentile of 0.336 (0% of permutations beat it) — and walk-forward out-of-sample holds up against in-sample. The signal carries genuine information; on gold over this window it just doesn’t convert that information into a positive expectancy after costs. Variant retired.

Gate scorecard — 4 / 11

| # | Gate | Result | Pass |

|---|---|---|---|

| 1 | ≥ 100 trades/periods | 259 trades/periods | ✅ |

| 2 | PF ≥ 1.20 net | PF 0.642 | ❌ |

| 3 | Annualized Sharpe ≥ 0.6 | Sharpe −0.84 | ❌ |

| 4 | Max DD ≤ 12% | MaxDD −50.8% | ❌ |

| 5 | Positive in ≥ 60% of years | 20% years positive | ❌ |

| 6 | Block-bootstrap 95% LB Sharpe > 0 | 95% LB Sharpe −1.38 | ❌ |

| 7 | Placebo: real PF > p95 | real PF 0.642 vs placebo p95 0.336 | ✅ |

| 8 | 2× cost stress: PF > 1.0 | 2x-cost PF 0.526 | ❌ |

| 9 | Deflated Sharpe positive | SR_hat −0.84 vs SR0 0.99, DSR=0.000 | ❌ |

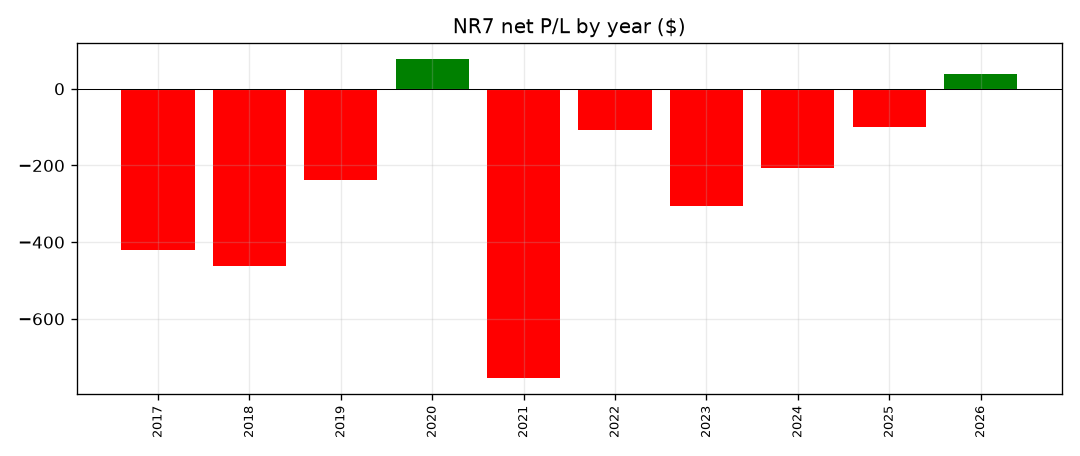

| 10 | No calendar year > 40% of P/L | max year share 28% | ✅ |

| 11 | Walk-forward OOS PF ≥ 0.9× IS | OOS/IS PF 1.38 (IS 0.60, OOS 0.82) | ✅ |

Gates evaluated on the base pre-registered config (stop = opposite side of the NR7 bar, 2R target, 1% risk at 1R, $0.40/oz round-turn cost). No configuration was selected post-hoc to pass.

Real signal, no profit

The two gates that usually kill a strategy — the placebo and walk-forward checks — both pass here. The placebo is decisive: 0% of random sign-permutations beat the real run, and real PF 0.643 sits well above the placebo 95th percentile of 0.336. Walk-forward is just as clean: OOS PF 0.82 actually exceeds IS PF 0.60 (ratio 1.38), so this is not an overfit in-sample mirage. NR7 compression genuinely marks bars that break with above-random follow-through.

But information is not edge. The same run fails every profitability gate: PF 0.642 (need ≥ 1.20), Sharpe −0.84, max drawdown −50.5%, only 20% of years positive, and a 2× cost-stress PF of 0.526 that collapses further under realistic slippage. The deflated Sharpe is effectively zero. The breakout fires correctly and still loses, because on gold over this window the 2R target and opposite-side stop give back more on the whipsaws than the genuine continuations pay. The signal is real; the net-of-cost expectancy is not.

Verdict: REJECTED (PF 0.643). Do not deploy. NR7 beats random and survives walk-forward — the compression signal carries information — but it is firmly unprofitable net of costs on XAUUSD: Sharpe −0.83, −50.5% drawdown, positive in only 20% of years. The variant is retired.

Charts & evidence

Frequently asked

Has the Crabel NR7 strategy been backtested honestly?

Yes. Toby Crabel's Narrow-Range-7 (NR7) volatility-compression breakout was run on gold (XAUUSD) over 2017–2026 through a pre-registered 11-gate battery. It passes only 4 of 11 gates: a profit factor of 0.643, a Sharpe of −0.83, a −50.5% max drawdown, and positive returns in only 20% of years. The compression signal does beat a random placebo, but the system is unprofitable net of realistic costs.

Is the NR7 breakout signal real or random?

The signal is statistically real but not profitable. NR7 passes the placebo gate — the real profit factor of 0.643 beats the random-permutation 95th percentile of 0.336 — and walk-forward out-of-sample performance holds up relative to in-sample. So NR7 compression carries genuine information, but on gold over this window it does not convert that information into a positive expectancy after costs.

Methodology: The Validation Gauntlet — pre-registered spec, 11-gate battery, real market data.

Full reproducible report: backtests/nr7_xauusd/results.json in the source repository.

Author: Brent Akamine (Founder, Vinovest). Backtests are not investment advice.